The “Registry Stuck” Reality: A Window of Opportunity vs. The Fear of Missing Out:

If you are hunting for a home in Noida Extension (Greater Noida West), Indirapuram, Crossing Republik, or along the Yamuna Expressway, you have likely encountered a confusing scenario. You find a premium, ready-to-move flat where families are already living, but the broker tells you: “The Registry (Sale Deed) is currently on hold.”

This is the reality for thousands of flats across the NCR belt. Whether due to builder dues pending with the Noida/Greater Noida Authority, ongoing NCLT proceedings, or delays in the Occupancy Certificate (OC), a formal government registry is paused.

The Market Paradox: Why Buyers Are Still buying

Because of this legal deadlock, these properties are often available at a price 30% to 50% lower than the prevailing market rate for registered properties.

The Fear Factor: Genuine end-users know that this situation is temporary. The government (including the Amitabh Kant Committee recommendations) is actively working to delink builder dues from homebuyer registries.

- The Risk: If you wait for the registry to open, property prices in these sectors will likely skyrocket, potentially making your dream home unaffordable.

- The Opportunity: Buying now allows you to lock in the property at today’s discounted price via a process called “Builder Transfer.”

The Roadblock: “Bank Says No”

Here is where the frustration begins. You are ready to buy, but when you approach a bank for a Home Loan, they reject the file.

- Why? Traditional Home Loans require a registered Sale Deed to create a mortgage. Without a registry, banks cannot create a charge on the property.

This is where Joy Loan steps in. We don’t look at the property papers for collateral; we look at you. Based on your profile, we offer a 2‑day fast loan for builder transfer property in Noida, Greater Noida, Noida Extension, and Ghaziabad.

🏗️ Understanding the Process: What is “Builder Transfer”?

To navigate this market, you must understand the terminology. Since a government Sale Deed isn’t possible yet, ownership changes hands through the Builder’s records.

People search for this using various terms, and we cater to all of them:

- Builder Endorsement / Transfer: The builder updates their ledger, replacing the Seller’s name with Yours. They issue a transfer or Endorsement Letter in your favor.

- GPA (General Power of Attorney): Common in certain pockets of Ghaziabad where the registry is stuck due to technical norms.

- Resale on BBA (Builder Buyer Agreement): You are technically buying the rights and interests mentioned in the original agreement.

- Transfer Memorandum (TM): The official permission from the Authority (often pending in these cases).

Note: While this is a standard market practice in NCR, it requires careful financial planning since traditional financing is absent.

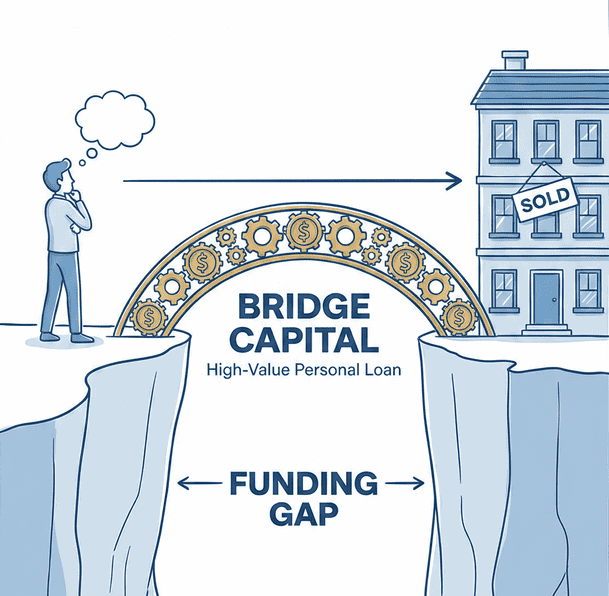

🚀 The Solution: “Bridge Funding” via Jumbo Personal Loans

Since you cannot mortgage the property, Joy Loan utilizes a specialized financial instrument: The High-Value (Jumbo) Personal Loan.

Think of this not just as a “personal loan” but as “Bridge Capital.”

How the Strategy Works

- Acquisition: You take an unsecured loan of ₹20 Lakhs to ₹5 Crores based on your income and repayment capacity.

- Purchase: You use these funds to pay the seller and complete the Builder Transfer/Endorsement process. You take physical possession and move in.

- Refinance (The Exit Strategy): You pay the EMIs for now. Once the registry opens in the future (1, 2, or 3 years later), the property becomes eligible for a standard Home Loan or Loan Against Property. We can then help you apply for a Home Loan to pay off the Personal Loan, drastically reducing your interest rate.

Get an instant assessment for ₹20 Lakhs to ₹5 Cr Unsecured Funding. No collateral required—just your income profile.

Key Features of Our Funding Solution

- ✅ No Collateral Required: The funding is based purely on your financial strength (Credit Score + Income), not on the property’s legal status.

- ✅ Massive Loan Cap: We facilitate loans up to ₹5 Crores with single or multi-funding arrangement.

- ✅ Flexible Tenure: Repayment options from 5 to 8 years, ensuring your monthly outflow is manageable.

- ✅ 2-Day Fast Disbursement: Once we receive the complete documents, we can facilitate the disbursement within two working days

- ✅ Top-Tier Lenders: We do not work with shady apps. We bring you offers from India’s most trusted financial institutions:

- Banks: ICICI Bank, HDFC Bank, Axis Bank, Kotak Mahindra, IDFC First, Yes Bank, HSBC, etc.

- Premium NBFCs: Bajaj Finance, Tata Capital, Aditya Birla, etc.

🤝 Why Trust Joy Loan? (We Are Strategists, Not Agents)

In a market filled with misinformation, Joy Loan stands as a pillar of transparency. We are not just loan agents who forward emails; we are Loan Strategists.

Our Legacy of Trust

- Since 2012: We have over a decade of deep experience in the Delhi NCR real estate finance market.

- 1,000s of Happy Customers: We have successfully funded families who are now happily living in their homes in Noida and Ghaziabad, even before their registry was done.

💡 The “Joy Loan” Advantage: Maximizing Your Eligibility

A common fear is: “My salary is ₹1.5 Lakhs. A bank will only give me ₹30-40 Lakhs personal loan. But the flat cost is ₹80 Lakhs. How do I buy it?”

Standard bank credit managers often look at your profile in isolation. We dig deeper.

1. Family Income Clubbing (The “Household” Approach) 👨👩👧👦 We don’t just assess your income. We assess the repayment capacity of your entire family.

- Example: You earn ₹1.5 Lakhs. Your spouse earns ₹80k. Your father receives a pension or has rental income (which he doesn’t file deeply in ITR).

- The Joy Loan Way: We present the “Total Family Income” to the lender to justify a higher loan amount, ensuring you get the full funding needed for the flat.

2. The Multi-Lending Strategy 🔄 If one bank has a policy cap of ₹40 Lakhs per individual, we don’t stop there. We intelligently structure your application across 2-3 compatible lenders simultaneously (e.g., ₹40L from first bank + ₹40L from 2nd bank). We manage the timing and documentation to ensure all loans are disbursed smoothly to meet the seller’s payment deadline.

3. Our Ideal Customer Persona This premium service is designed for:

- Salaried Professionals (MNCs, Pvt Ltd, Govt).

- Net Monthly Salary: ₹1.25 Lakhs+

- Credit Score (CIBIL): 740+ (Mandatory for unsecured funding).

Don’t settle for less. We specialize in clubbing family income to maximize your loan limit. Trusted by 1000+ Delhi NCR homebuyers.

🏘️ Targeted Locations & Projects: Where We Can Help

The “Registry Stuck” issue is specific to certain developer pockets. We have successfully processed funding for “Builder Transfer” cases in:

1. Noida & Greater Noida West (Noida Extension)

- Amrapali Group: Specific focus on projects under NBCC/Court Receiver supervision (Silicon City, Princely Estate, Zodiac, etc.). Note: Since the Supreme Court is monitoring these, buyers feel safer, and we provide the funding.

- Jaypee Infratech: Wishtown, Kensington Park, Kosmos, Klassic.

- Unitech: Unihomes, Uniworld (Noida & Gurgaon).

- Supertech: Eco Village series, Cape Town, Romano.

- Logix Group: Blossom County, Zest.

- Other Key Developers: Ajnara, Mahagun, Gaur (Specific phases where OC is pending).

2. Ghaziabad (NH-24 / Raj Nagar Extn)

- Crossing Republik Townships: Resale cases where the registry is on hold.

- Indirapuram: Specific parcels involving builder dues.

🛡️ Safety First: A Checklist Before You Apply

While we handle the finance, we want to ensure your hard-earned money goes into a safe asset. If you are buying a “Builder Transfer” property, you must verify:

- No Dues Certificate (NDC): Demand a current NDC from the builder. Alternatively, ask for the Builder Ledger Statement to ensure the seller has paid all construction-linked demands.

- Physical Possession: Do not buy “on paper” possession. Ensure the flat is ready, and keys are handed over immediately upon transfer.

- The “Transfer” Cost: Clarify who pays the transfer charges to the builder (typically ₹100-₹200 per sq. ft). This should be negotiated before the deal.

- Court Status: In NCLT cases (like Jaypee/Amrapali), keep an eye on the latest Supreme Court directions regarding homebuyer rights.

🗣️ Frequently Asked Questions

No, traditional home loans require a registered sale deed. However, Joy Loan can arrange a “Jumbo Personal Loan” which acts as bridge funding to buy the property now.

Thousands of buyers are transacting in Amrapali projects under the supervision of the Court Receiver. While we cannot give legal advice, we provide the funding (Loans) to enable these purchases for creditworthy buyers.

Rates start from 9.99% (Reducing balance) for customers with a CIBIL of 750+. While higher than a home loan, it allows you to secure a property at a much lower price point.

Depending on your income and CIBIL profile, we can arrange anywhere from ₹20 Lakhs to ₹5 Crores through our multi-bank channel partners.

📞 Don’t Let a Paperwork Delay Stop Your Home Purchase

The window to buy these properties at 2018-2020 prices is closing. Once the registry opens, the affordability factor may vanish.

If you have identified a property and have the income profile to support it, don’t let a “No” from a bank stop you.

Get an Expert Assessment Today. Let us evaluate your profile, calculate your “Family Funding Eligibility,” and connect you with the right lenders from our network.

👉 [Check Your Jumbo Loan Eligibility Now] (2-day-fast disbursement. 100% Transparent Process.)

Beat the price hike. Fast & transparent processing for Amrapali, Jaypee & Builder Transfer cases in Noida/Ghaziabad.