Processing Fee of HDFC Home Loan V/S SBI Home Loan

On face of 2 home loan offer, one may look better than other. As a customer, you are concerned about rate of interest bank will charge. There are small details if you miss, can make you pay your home loan for up to 25% longer time. Unbelievable?

Then believe me. I too got surprised, when I entered values in EMI calculator for making tables and charts for this post. Though it is small choice, but it has far reaching consequesnces. These small details are not to be missed, if you want to not get fooled.

In Continuation of last blog HDFC V/S SBI Which is Better for Home Loan (9.6% V/S 9.55%). Exciting update for you is, this week HDFC Home Loan has reduced its rate of interest in festive offer. If you are planning for home loan or transfer your home loan, you can get @ 9.55% ROI from both HDFC Home Loan and SBI Home Loan. Additionally if you are female or your co-applicant is female you can get additional discount 0.05% on ROI.

We are putting some research to find out how much you pays to get this deal. So at the end which is winning deal for you.

After you have taken home loan, you pays only interest on outstanding principal amount. So our focus is only for charges you pays before you take home loan. There are 2 initial expense to get home loan

- Insurance Charges

- Total Processing Fee

1. Insurance Cost for Home Loan

Cost of insurance is big initial expense for you while taking home loan. Here important fact is, SBI will not disburse home loan without taking its SBI home loan protector from SBI Life Insurance as well as SBI general insurance. To get SBI Home Loan taking both insurance is mandatory. I will be discussing, further in details how much this will costs you. You will also learn, is it profitable to spend that much amount for loan deal which is almost equal to other home loan providers.

On other hand like SBI, HDFC too has its subsidiary companies for Life as well as general insurance. But they don’t force this cross sell to it’s home loan customer. You can look below for pro and cons of Home Loan protector and decide if the price of its benefit right for its cost?

Plus points of taking home loan protector

- Single premium for entire loan tenure (Paid at starting)

- It gets financed over and above loan value from institutions

- Most of time it gets issued without undergoing medical test

Negative points of home loan protector

- It is costly than normal term plan

- You can not transfer loan protector in case of home loan balance transfer to other lender

- Premium is charged based on outstanding loan amount in normal payment condition

- Part Payments are not taken into consideration

- When you makes part payment, your home loan protection premium does not reduces

Yes to me, first point for not suggesting a loan protector is its cost. It is really very costly compared to a normal term plan. Depending on your age, its premium can range between 4% – 9% of loan amount.

In some other blog, I will explain your why home loan protectors are expensive than term plan. Why they are being sold and who is selling them.

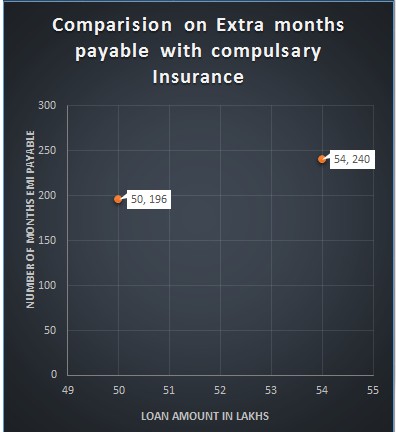

Fact is, to be able to make down payment and pay EMI stably, age of general customer is more than 35 years. If you started all by yourself, & you are a self made man / woman possibility may be your age is 40 years or more. Entering in to Home loan protector insurance plan at your age can make you pay roughly 8% of loan amount. I have given here a table as well as a chart, to showcase how much longer you will have to pay if you choose loan protector.

Over here I have shown a example of “A” who is 39 year old. He has taken home loan of 50 Lakhs from SBI with compulsory loan protector with premium of 8% of loan value( 4Lakhs). On other hand “B” has taken 50 Lakhs loan from HDFC which without home loan protector

[supsystic-tables id=”15″]

It is clear “A” is paying slightly higher EMI than “B”. But A will pay for 20% – 25% longer tenure. Check out EMI Calculator below and find out how much longer your loan protector can make you pay for your home loan.

| Powered by Mortgage Calculator Auto Loan Calculator |

Here I found few experts in financial sector telling the almost same thing. They may have different logic but the crest of the matter is same. Nobody recommends home loan protector over term plan.

- Nitin Bhatia Blog

- Curious Logic Blog (Link removed on December 28th, 2018 as Curious Logic website has stopped services)

[mc4wp_form id=”1322″]

2. Total Processing Fee for Home Loan

To make easy for you to understand, I am considering all charges including bank PF, valuation charges and legal charges from advocate all as “Total Processing Fee”. I will be discussing step by step Total Processing Fee for different loan amount, based on profile. I.e. Salaried and self-employed. So you can check which is most relevant to you

If you are a NRI / PIO HDFC Home Loan will charge you PF as per salaried grid. So if you want to take a Home loan in India as NRI / PIO, then HDFC Home Loan is sure a better option because of their worldwide presence with office located specifically to serve home loan customers.

Processing Fee structure of HDFC Home Loan V/S SBI Home Loan

SBI Home Loan PF is based on loan value. Following are SBI Home Loan PF for different loan amount

[supsystic-tables id=”13″]

HDFC Home Loan PF is based on loan value as well as customer profile. Following are HDFC Home Loan PF

[supsystic-tables id=”14″]

For you I have done detailed comparison of Total Processing Fee for different loan amount with different profile. Salaried, Salaried NRI / PIO, Self Employed Professionals. Check below as per your profile. As legal charges are payable direct to law firm in both cases, I have not taken legal charges for comparision which are almost similer in both cases

[expand title=”Push For Salaried” trigclass=”noarrow my_button” targclass=”my_content” tag=”div”]

I have strategically shown here case size of loan amount 10 lakhs, 25 Lakhs & more than 75 lakhs.

Reason for choosing 10 lakh is HDFC Home Loan & SBI Home Loan charges PF 0.5% & 0.25% respectively. It was appropriate to showcase how they compete in PF segment for small loan amount.

Reason for choosing 25 lakhs is HDFC Home Loan has maximum capping of 10000/- & SBI Home Loan changes its next PF slab on 25 Lakhs loan amount. We wanted to show how PF of both financial institution works in loan amount at this range when HDFC Home Loan has gone for its maximum PF, but SBI Home Loan is still offering its middle slab of PF.

Reason for choosing 75 lakhs is both HDFC Home Loan as well as SBI Home Loan are charging same PF which is 10000/- we have showcased their consolidated charges for loan amount more than 75 lakhs

[/expand]

[expand title=”Push For Self-employed” trigclass=”noarrow my_button” targclass=”my_content” tag=”div”]

For your business profile I have chosen to take example of higher loan amount. My purpose for choosing higher loan amount is, for smaller loan value, you will have to pay almost same PF with HDFC Home Loan and SBI Home Loan. For bigger home loan amount, difference between Processing Fee of HDFC Home Loan and SBI Home Loan becomes wider

[/expand]

If you found this blog useful, please share. Or if you have some quarry, please comment below. I will revert to you soon

Hi Sir, Thanks for this useful information it is really helpful will recommend to others as well but for my SBI home loan application they took around 3 months and misguided me in some area,Is it mandatory to take property Insurance as I took home loan for 10.00lac with SBI.

HI Sandeep!

Insurances are always optional but nowadays many institutes do hard selling on this due to additional revenue

good info

Thanks Hanif!