High-Value Unsecured Personal Loans (₹50L to ₹5Cr+)

Dreams… made real

Check My Eligibility for ₹50L+

Joy Loan is a trusted capital intermediary. We operate with absolute privacy. We do not underwrite subprime profiles, active defaults, or recent payment delays.

Jumbo Loan Limits

₹50L to ₹5Cr+ with zero property dependencies.

Starts @ 9.98% p.a.

Sourced from 50+ banks. Best-deal guarantee.

48-Hour Disbursal

100% digital workflow. Zero branch visits required.

8-Year Tenure

Up to 96 months for manageable cashflow.

Flexible Structure

Part-payments and foreclosure allowed after 12 months.

Why Joy Loan

Parallel Credit Engineering

Simultaneous banking logins maximize overall funding limits.

Experienced Loan Strategists

Bypassing broker channels for direct committee approvals.

Ironclad Absolute Privacy

Strict discretion for corporate executives and specialists.

14+ Years Trust – Since 2012

Sourcing premium capital for thousands since 2012.

Pan-India Processing

Serving Delhi NCR, Tier-1, and Tier-2 cities.

Let our experts find the best loan for your unique profile.

Banks / NBFCs We Deal With…

*We are independent consultants. We do not represent or act on behalf of any bank. Logos are not used to imply affiliation.

We connect you with the right lender for your needs.

Architectural Capital: Who We Engineer Capital For

Standard banking frameworks use automated algorithms that treat a corporate leader or specialist doctor like a generic retail applicant. At Joy Loan, we operate as Loan Strategists, building custom capital pathways for distinct elite profiles across India’s economic hubs:

- Corporate Leadership (CXOs, VPs, & Directors): Structured for high-earning executives in Tier-1 hubs (Delhi NCR, Mumbai, Bangalore, Hyderabad) who require massive liquidity without liquidating equity or disrupting wealth portfolios.

- Consultant Doctors & Medical Specialists: Designed for senior medical specialists at premier hospital networks (e.g., Max, Medanta, Apollo) who balance a fixed salary with private practice cash flows, requiring seamless debt consolidation or immediate clinical expansion funds.

- NCR Real Estate Buyers (Stalled Registries & GPA Plots): Tailored for professionals caught in complex property loops in Delhi, Noida, Greater Noida, and Gurugram. When traditional home loans fail due to builder transfer delays, unapproved farmhouse plots, or GPA title chains, we secure capital based entirely on your high salaried profile.

- Global Indian Professionals (NRIs & Merchant Navy Officers): Specialized processing for maritime professionals and NRIs. We factor in multi-currency income streams, contract continuity, and offshore remittances, enabling execution from anywhere globally with deployment ready upon landing in India.

We structure complex incomes to meet your fund requirement.

Mandatory Institutional Underwriting & Eligibility Floors

To maintain our streamlined, high-velocity relationship with senior credit managers, applicants must meet these strict underwriting criteria:

- The Credit Floor: A strict CIBIL score baseline of 740+ is standard for prime turnaround. Conditional exceptions between 710 and 740 are handled exclusively for applicants with exceptional job stability and document backed justification. Profiles below 710 are automatically filtered out.

- The Income Floor: Minimum net salaried earnings of ₹1.5 Lakhs per month (₹18 Lakhs+). Applicants must possess a minimum of 1+ years of stable employment within MNCs, reputed private limited companies, hospitals, or government cadres.

- Age Requirements: Salaried professionals between 23 and 55 years old.

🛑 Joy Loan operates exclusively as a capital strategist. We do not underwrite subprime applications, active defaults, or profiles with recent delayed payments.

Simplify your finances with one smart move.

Strategic Applications of Jumbo Unsecured Capital

High-net-worth buyers and senior corporate professionals frequently utilize our high-ticket capital access as an efficient unsecured bridge loan for property purchase. This approach is highly effective when traditional home loans and commercial property purchase loan face delays or outright rejection due to non-standard legal or technical property issues.

1. Financing and Constructing Highly Discounted GPA Properties

Outstanding real estate deals often require purchasing a property via General Power of Attorney (GPA) transfers. Because banks completely refuse home loan on GPA properties, savvy buyers utilize an unsecured personal loan 50 lakhs or higher to settle with the seller in cash and secure the asset safely.

This issue is highly prevalent across the Delhi NCR region. In Delhi, numerous prime residential and commercial locations face immense financing challenges due to GPA titles. Banks and NBFCs do not offer funding for purchasing or building on these properties. Joy Loan bypasses this friction entirely; because our underwriting is based 100% on your salary. You can use the capital for both the purchase and the subsequent construction of GPA property without property inspection.

2. Rescuing Registry-Stalled Builder Transfer Flats

In key growth corridors across Noida, Greater Noida, and Greater Noida West (Noida Extension), thousands of completed, high-value apartments face frozen registries due to long-standing developer-authority lease rent disputes. If you locate an undervalued resale deal inside these premium residential societies, traditional home loans are impossible to obtain. A jumbo unsecured capital line allows you to pay the seller (or builder), manage the internal builder transfer, and acquire the flat instantly while waiting for the local administration to resume formal registrations.

3. Acquiring Unapproved Land, Plots, and Farmhouses

Purchasing highly affordable suburban land parcels, non-municipal plots, or strategic agricultural tracts with immense growth potential requires immediate liquidity. Because standard banking channels will not issue a traditional home loan or Loan Against Property (LAP) on unapproved layouts, a high-value personal loan bridges your entire capital gap seamlessly, protecting your personal investments from external delays.

4. Strategic High-Income Debt Consolidation

High earners with multiple active car loans, short-term personal credit lines, or fragmented credit card balances frequently find their monthly cash flows heavily strained by mismatched payment schedules. We execute a tailored personal loan for debt consolidation high income program, wiping out your smaller liabilities completely and merging your entire debt footprint into a single, structured, low-interest capital line with a single manageable EMI.

5.Specialized High-Value Lines for NRI & Merchant Navy Professionals

Obtaining a jumbo unsecured capital line above ₹50 Lakhs can be exceptionally difficult for offshore professionals and seafarers. Most mainstream automated bank algorithms flag rolling maritime contracts, and extended voyage gaps as high-risk compliance exceptions.

Joy Loan bypasses standard automated retail rejections through specialized underwriting models. We evaluate your eligibility based on your last contract income, continuous discharge certificates (CDC), and consistent NRE/NRO account remittances to present annual income footprint directly to senior credit managers.

🛑 Important Compliance Note: Formal bank login requires your physical presence in India. For Merchant Navy and NRIs personal loans, arrival immigration stamp is required alongside your core loan documents. However, we can initiate complete pre-screening of your loan eligibility ahead of time. This ensures your loan application is perfectly ready the moment you touch down on shore.

👉 [Explore Our Dedicated Merchant Navy & Seafarer Capital Programs]

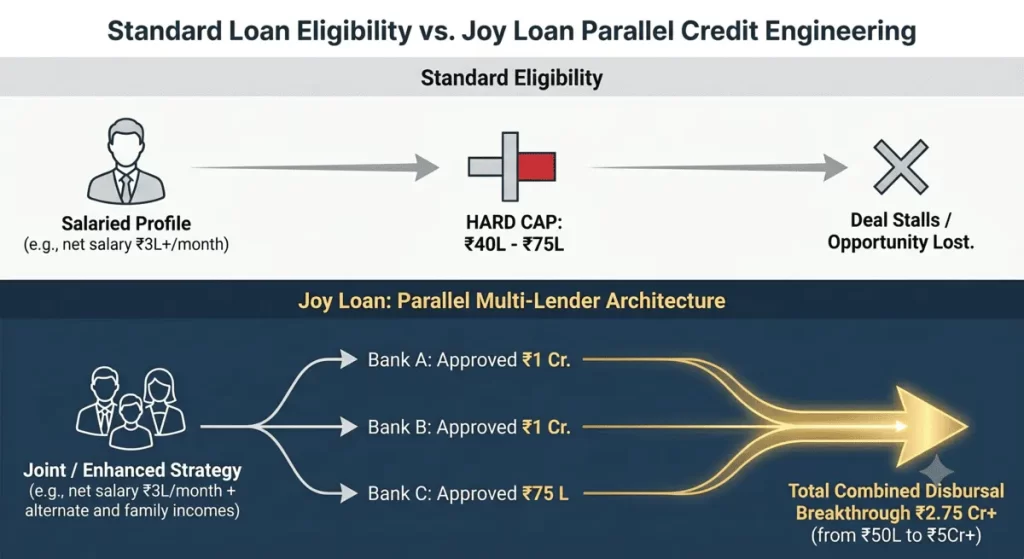

Overcoming the Single-Bank Limit: The Parallel Multi-Lender Strategy

If you earn a substantial income (such as ₹3 Lakhs to ₹5 Lakhs+ per month), a traditional bank’s automated retail algorithm will still cap your unsecured loan limit. They limit it between ₹40 Lakhs and ₹75 Lakhs due to internal retail risk guidelines. If you need ₹1.5 Crores to acquire a highly discounted property or a prime plot of land, retail desk of a single banking institution cannot fulfill your true requirements.

Joy Loan resolves this limitation through expert profile matching and comprehensive pre-login discussions directly with the senior credit team. This hands-on process allows us to negotiate the highest personal loan amount for salaried individuals at the most competitive interest rates.

Unlocking Higher Capital via Family Repayment Capacity

When your funding requirement exceeds the standard eligibility rules of a single lender, we deploy our proprietary Parallel Multi-Lender Architecture. Instead of submitting a single application, we break down, structure, and submit your profile across 2 to 3 shortlisted banks simultaneously.

By coordinating these institutional timelines, we blend separate banking limits into a single, cohesive capital line ranging from ₹1 Crore to ₹5 Crores+.

To achieve a higher-than-normal eligibility rating, our credit specialists run an enhanced assessment of the total repayment capacity of your family. We factor in secondary income channels, including:

- Salary of other family members

- Rental inflows

- Income from family business

This specialized credit wrapping ensures you secure the capital you need while keeping your income to EMI ratio manageable.

Our loan expert helps structuring the highest loan based on your family repayment capacity.

FAQs High-Value Personal Loans

Q: What is the absolute maximum loan amount for salaried person profiles based on market regulations?

A: There are no market regulations restricting loan amount. Yet bank limit retail loan borrowers to ₹40 Lakhs to ₹75 Lakhs to control risk. However, the true maximum loan amount for salaried person applicants is governed purely by their Fixed Obligation to Income Ratio (FOIR).

By utilizing Joy Loan's expertise, and direct discussion with senior credit team, you can be eligible for up to 3Cr from single bank. If you have higher salary or additional family income, we can process your loan with 2-3 shortlisted banks simultaneously. This allows creditworthy high-income earners to pool multiple non-conflicting limits and unlock up to ₹5 Crores+ in clean liquidity.

Q: What are the minimum eligibility criteria to unlock a personal loan above 1 crore?

A: To cross the personal loan above 1 crore eligibility threshold without providing collateral, you must present:

1. Minimum net monthly salary of ₹1.5 Lakhs or higher, backed by a family income profile of ₹3 Lakhs+ per month.

2. Strong CIBIL score baseline of 740+

3. Sustainable existing debt-to-income ratio.

4. 1+ year of work experience within a top-tier private corporate entity, MNC, premium hospital, or government office.

Q: What minimum CIBIL score is required for high-value personal loan eligibility?

A: A minimum CIBIL score of 740 is required for high-value personal loan eligibility. To unlock the most competitive interest rates—often below 10.5%—lenders generally prefer a prime credit score of 760 to 800+. If your score sits between 720 and 740, approval is still highly achievable through our network, though the underlying interest rate bands may shift upward.

Q: Can I take a jumbo personal loan to purchase real estate if the property lacks a clear title chain?

A: Yes. Traditional home loans require a flawless property title chain and clear local municipal registry status. Because a high-ticket personal loan is 100% unsecured, institutional lenders evaluate your personal income, corporate employer classification (company listing), and financial stability rather than the property itself. This makes it an exceptionally effective bridge funding tool to buy highly discounted properties that standard home loans refuse to finance.

Q: Can I get an unsecured loan to buy unapproved agricultural land or a farmhouse plot in Delhi NCR?

A: Absolutely. Mainstream banks strictly prohibit regular mortgage or Loans Against Property (LAP) on unapproved locations, agricultural land tracts, or peripheral farmhouse plots. By securing a high-value personal loan based entirely on your monthly salary, the land's structural mapping becomes entirely irrelevant to the lender. This gives you immediate cash liquidity to secure affordable, high-growth land deals before prices escalate.

Q: How quickly can funds be disbursed for urgent property transactions, including an unsecured bridge loan for property purchase?

A: Unsecured capital can be disbursed within 48 to 72 hours for urgent property transactions and registry rescues. Because our complete intake processing framework is entirely digital, initial institutional credit approvals can be secured in as little as 8 hours. For pre-approved high-income profiles, same-day or next-day direct fund transfer to your salary bank account is common.

Q: I am a consultant doctor balancing a hospital panel salary with private clinic income. How does Joy Loan calculate my eligibility?

A: Traditional lenders typically review only your primary salary slip, discarding your secondary clinical income as volatile. As specialized Loan Strategists, we run a hybrid assessment model. We present your hospital salary credits alongside your clinic’s income tax returns (ITRs showing ₹10–20 lakhs+ annually) to present a unified financial profile.

By analyzing your aggregate cash flows rather than isolated streams, we expand your Fixed Obligation to Income Ratio (FOIR), allowing you to unlock premium credit lines up to ₹3 Crores to ₹5 Crores from top-tier institutions like HDFC, ICICI, or Axis Bank.

Q: I am a salaried professional (or NRI / Merchant Navy officer) based outside Delhi NCR (e.g., Mumbai, Bangalore, Chennai). Can Joy Loan manage my high-value personal loan application?

A: Yes. We handle outstation high-value unsecured personal loan cases seamlessly across all major Tier-1 and Tier-2 cities in India through a highly coordinated institutional network protocol. This standard procedure ensures that any high-value salaried professional, NRI, or Merchant Navy officer can leverage our centralized credit expertise regardless of their physical location in India.

Whether you are an IT Director in Bangalore, an MNC executive in Mumbai, or a senior corporate leader in Chennai, our onboarding infrastructure is completely digital. Identity mapping, financial scrubbing, and e-KYC verification are executed via secure online channels, bypassing physical branch dependencies and achieving direct account disbursal within 48 to 72 hours.

Q: Do you provide specialized personal loan paths for senior Defense and Army personnel?

A: Yes, commercial banks extend preferential interest rates and fee structures to both central government and defense officers.

Processing relies on your official department service certificate alongside standard income credentials. However, approval is subject to field-verification parameters. Private bank risk frameworks require physical verification agencies to clear the applicant's current base location. For example, a senior officer stationed at a base in Delhi NCR, Jammu, or a major Tier-2 cantonment will achieve smooth approval. Conversely, if you are currently deployed to a remote frontier zone in Kashmir where field verification is impossible, the application will face structural constraints.

Q: What documentation is required for high-value executive compensation verification and a salary-based GPA property loan?

A: To process your digital application seamlessly from any Tier-1 or Tier-2 hub across India, your dedicated strategist will require the following digital copies:

- Photo, Pan Card, Aadhar Card (additional current address proof require if Aadhar has other mentioned address)

- Latest 3 months’ salary slips

- Previous financial year’s Form 16

- Updated 6 months’ salary account statements

(Note: All digital intake data is handled via encrypted channels to maintain total executive privacy).

Specialized Documentation for Global Profiles:

If you are an elite professional working outside standard local frameworks, we require these additional documents to ensure your global income is counted:

- For NRI Applicants: Along normal resident documents (mentioned above), NRIs requires current employment contract letter, passport with work permit / visa stamp, and the latest 6 months of your NRE/NRO bank account statements.

- Maritime/Merchant Navy Personnel: Along with normal resident and NRI documents seafarers require CDC (Continuous Discharge Certificate) book entries for the last 3 years. (for sailing logs).

- Mandatory Indian Co-Applicant: Photograph, PAN card, and Aadhaar card (essential local contact point for NRI and Merchant Navy applications)

🛑 Important Compliance Note: Formal bank login requires your physical presence in India. For Merchant Navy and NRIs personal loans, arrival immigration stamp is required alongside your core loan documents. However, we can initiate complete pre-screening of your loan eligibility ahead of time. This ensures your loan application is perfectly ready the moment you touch down on shore.

Q: How do foreclosure, prepayment options, and lock-in periods operate for unsecured high value personal loans?

A: Standard retail personal loans carry rigid 12-month lock-in periods alongside flat 2% to 5% penalties on the residual balance. However, for jumbo unsecured facilities exceeding ₹50 Lakhs, we negotiate bespoke terms directly with senior credit committees.

Many of our institutional partners waive foreclosure charges entirely for high-ticket profiles once the initial lock-in clears. Additionally, while standard personal loans rarely permit part-payments, we intentionally route your profile to specific lenders that provide part-payment options with zero fee penalties, giving you total cash-flow flexibility.

Q: From which specific banking institutions will my unsecured capital be sourced?

A: Your unsecured capital is engineered and sourced from India's premier Tier-1 banks and top-rated NBFCs. Depending strictly on your corporate listing, income matrix, and credit profile, we route and match your application to institutions such as HDFC Bank, ICICI Bank, Axis Bank, HSBC, Kotak Mahindra Bank, Yes Bank, Standard Chartered, Tata Capital, and Bajaj Finserv to isolate the lowest interest rate offer.

Q: What is the processing fee for a high-value personal loan, and does Joy Loan charge a fee?

A: Institutional processing fees vary by lender; some banks charge a flat upfront fee (such as HDFC Bank at ₹5,999 or ICICI Bank at ₹7,999), while others deduct a small percentage of the total loan amount during final disbursement. Joy Loan charges absolutely zero fees to our customers for structuring, processing, or negotiating unsecured personal loans.

Q: How does Joy Loan protect client confidentiality during high-ticket loan processing?

A: We enforce absolute transaction privacy through dedicated, discreet processing channels. Your financial profiles, corporate credentials, and documentations are routed directly to senior credit committees through secure channels. This prevents unnecessary market exposure and ensuring complete professional discretion from sourcing to final disbursal.

Get expert assistance for higher loan—get a free eligibility check.

What Sets Joy Loan Apart:

- Highly Competitive Rates: Sourcing optimal interest rates starting at 9.99% p.a. from a network of 50+ leading banks and NBFCs.

- Unrivalled Repayment Flexibility: Flexible repayment tenures extending up to 8 years (96 months) to comfortably align with your cash flows.

- Early Foreclosure Paths: Clear, transparent part-payment and foreclosure options accessible after 12 months (*lender specific terms applicable).

- Streamlined Digital Processing: Complete capital disbursal within 2 to 3 business days via a secure digital workflow with minimal documentation and zero physical paperwork friction.

- Expansive Service Footprint: Service coverage across the entire Delhi NCR area, alongside major Tier-1 and Tier-2 economic cities including Mumbai, Bangalore, Pune, and Hyderabad.

Take the Next Step

Do not let rigid banking or non-standard property titles stand in the way of your financial growth or real estate plans. Let our senior credit strategists map out your parallel funding route today.

Apply anytime, anywhere—your loan is just a few clicks away.

Get Expert Assistance for Higher Loan at Best Terms

high-five with right team…

Simplify Your Finance!